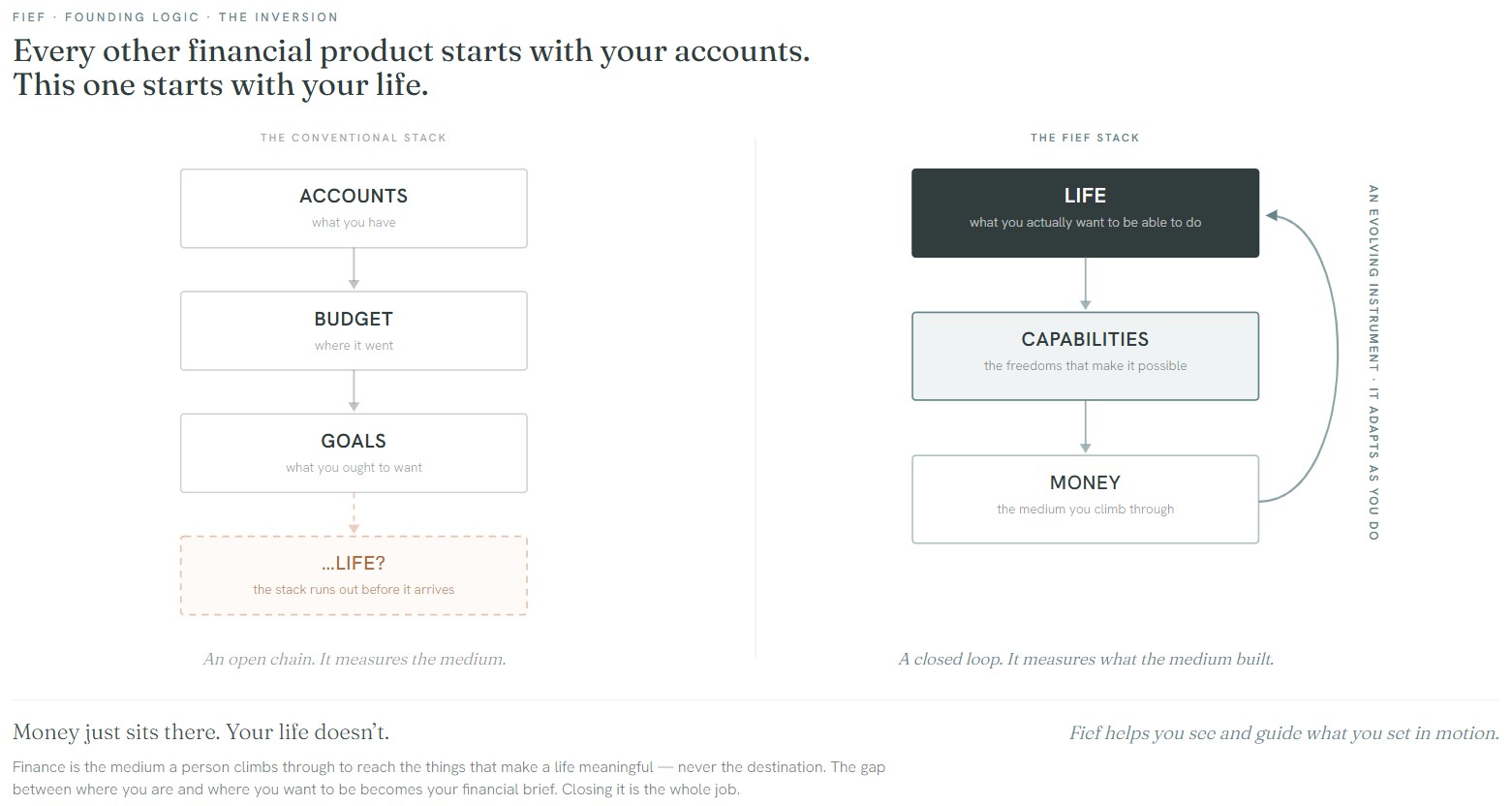

Start with the life, not the accounts

Every financial product built before Fief opens with your balances. Fief opens with a different question — what do you actually want to be able to do? Provide for someone you love, leave a job that's grinding you down, absorb a $400 shock without panic, put down roots. The distance between that and where you are now becomes your financial brief, and closing it is the whole job.

Every other financial product starts with your accounts. This one starts with your life.

The problem isn't that people are bad with money

The failure is emotional, structural, and categorical at once:

The shame loop

People open today's budgeting apps, then churn — they show the problem without a way out, so anxiety curdles into abandonment.

Losing ground, broadly

In the US, it's not one group. Younger adults, lower-education households, and Black and Hispanic families are all sliding to multi-year lows — while a flat national average hides it.

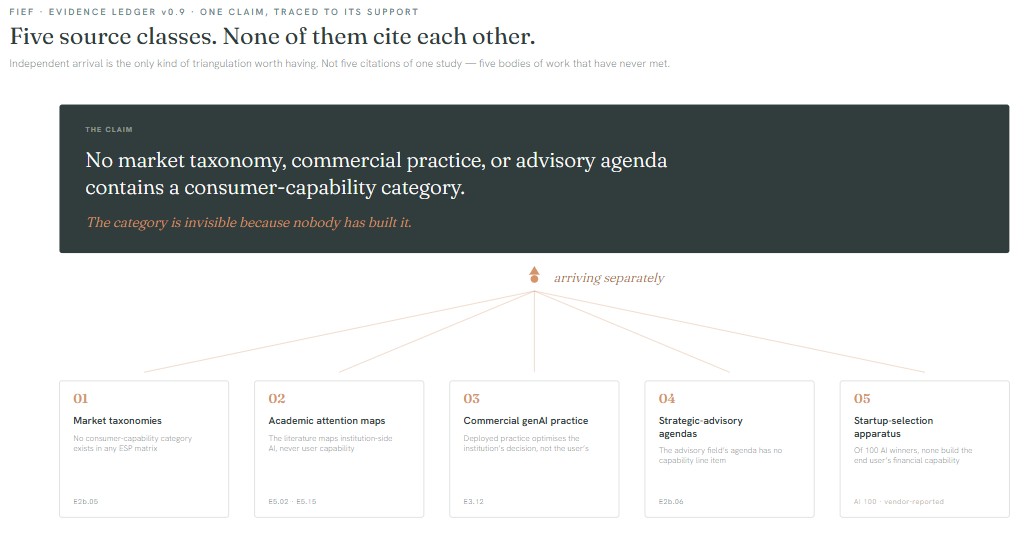

An empty category

Capability-as-core is unoccupied — not even a keyword across five independent source classes.

“I know I should be doing more, but every time I open my bank app I just feel overwhelmed and close it.” — survey respondent

Grounded in contextual evidence

I built the instruments to avoid deficit and shame language, so the research surfaced what people want to build — not just what they lack. Every claim in the deck traces back to a numbered source.

Find the field no one else is on

A Blue Ocean canvas scored six evidenced competitor segments. Fief's field — capability-as-core, shame-free, decision-agency — sits uncontested.

Not weak demand

Capability-as-core is absent across five source classes; PFM apps top out under $1B while adjacent capital magnets sit 50–180× higher.

Partnered, not paid

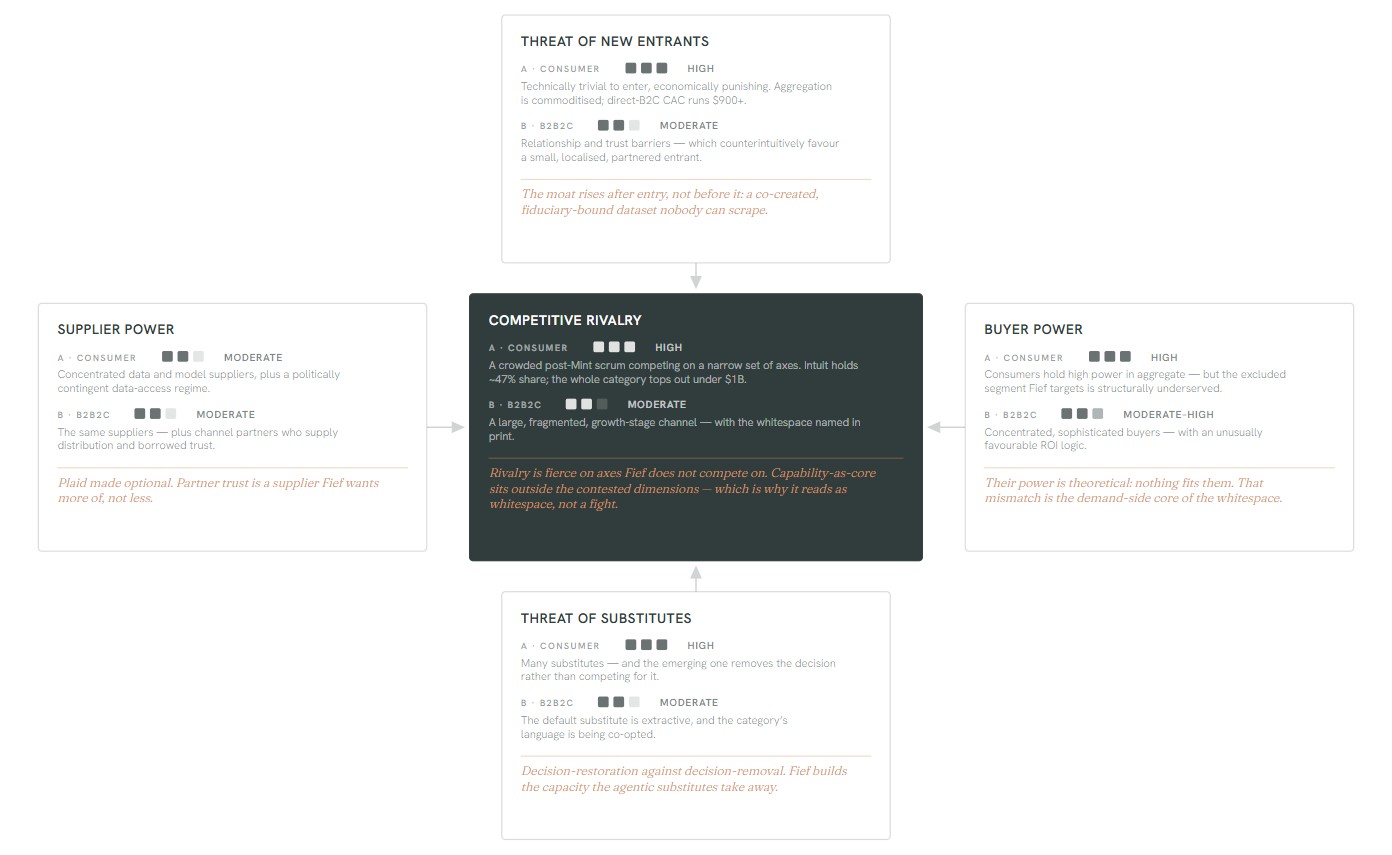

Porter's dual-lens points to a B2B2C entry through employers and community FIs — beating a $900+ direct-to-consumer CAC.

Unscrapeable

Co-created fiduciary data, “decision restoration” against an industry automating the choice away, and user-side “Know Your Agent.”

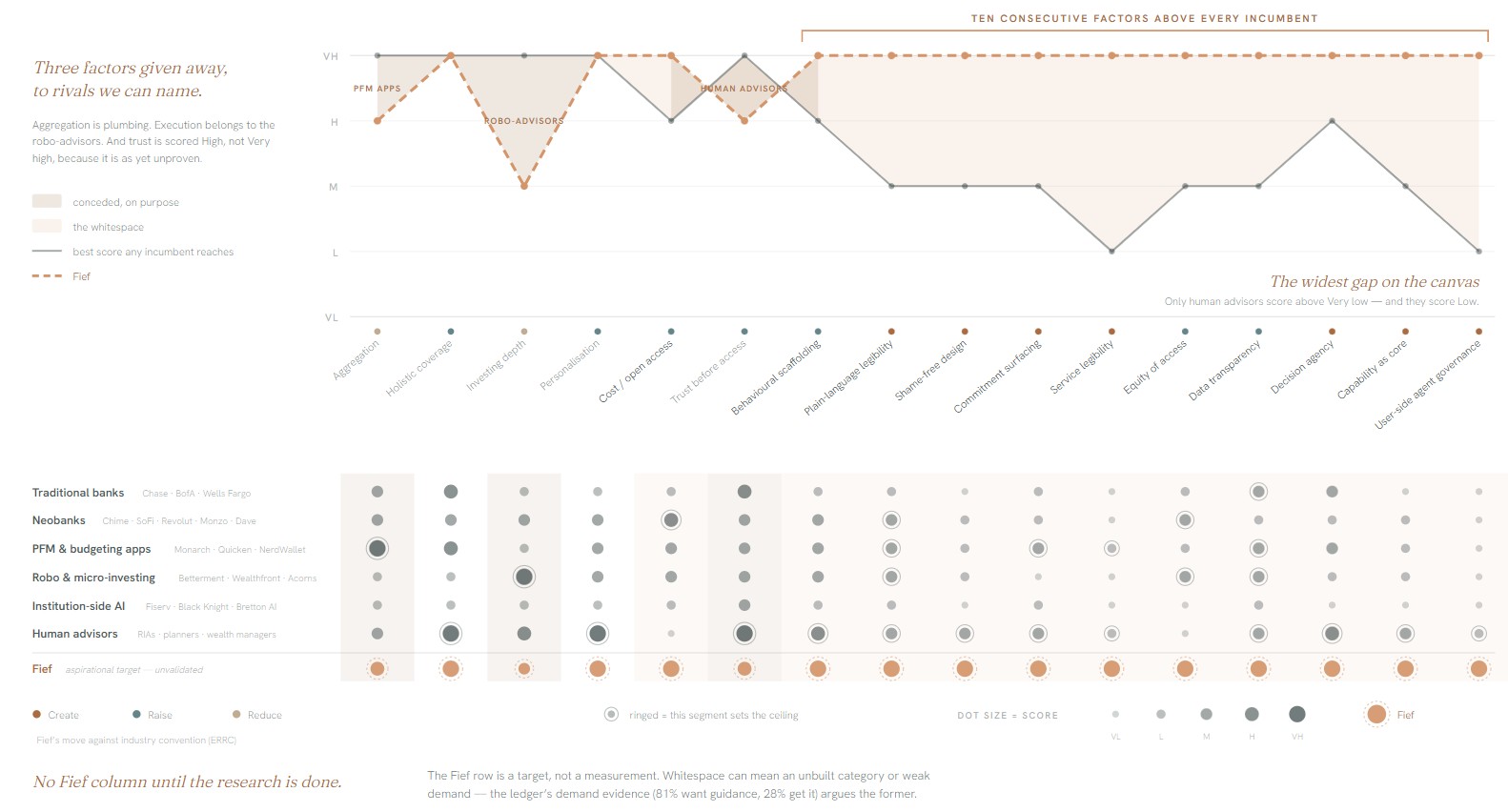

Fief's own value-curve position is shown as an aspirational target — pre-validation.

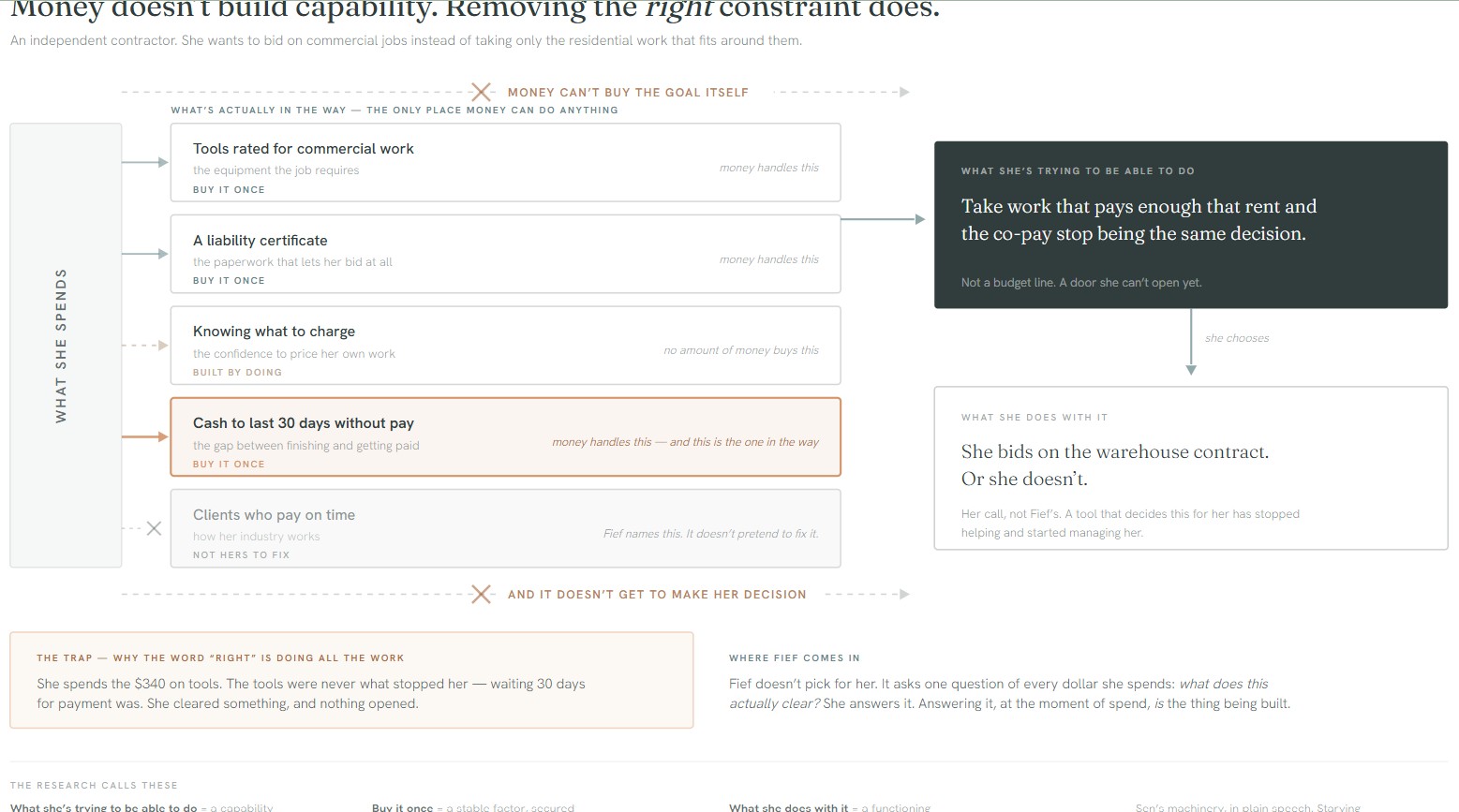

What money is actually for

Money doesn't build capability. Removing the right constraint does.

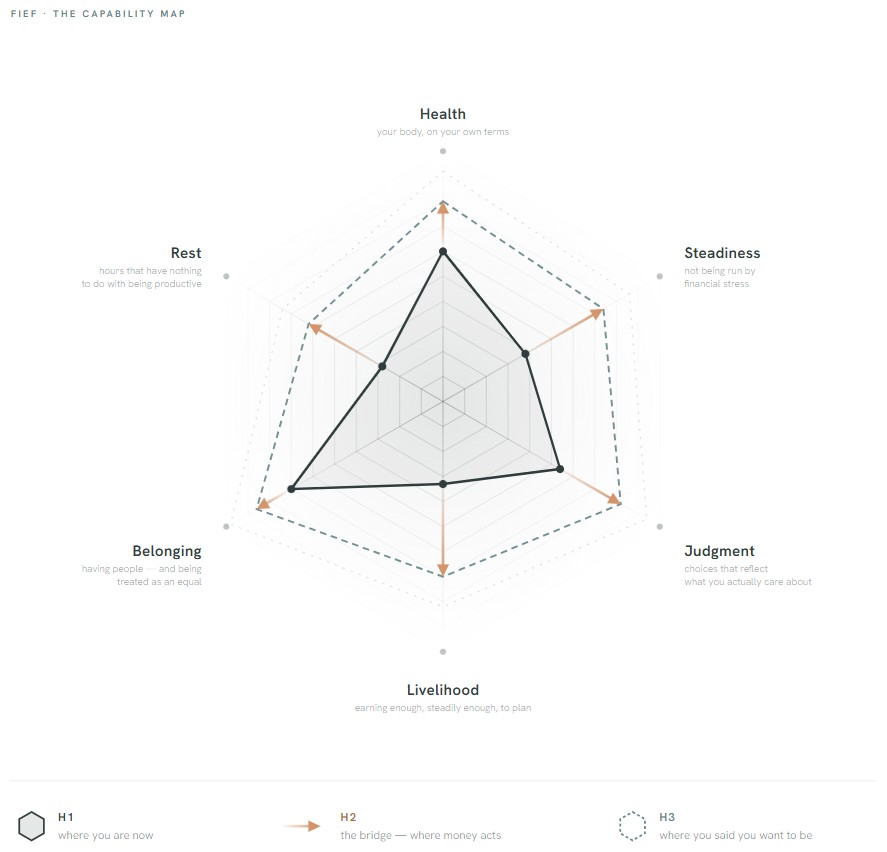

Built on Nussbaum and Sen's capabilities approach: the map's axes are capabilities (freedoms to do or be); money acts on the conversion factors — the buffer, the knowledge, the access — that gate them; functionings are the outcomes you actually choose. Every spend gets read as product, service, or hybrid: does it amplify capacity, or create dependency?

Classifying is the build

Naming what a flow builds is itself a capability-building act — and doing it at the moment of spend is where it carries the most leverage.

From “what did I spend” to “what is my money building”

The cognitive pivot that breaks the budgeting-category collapse.

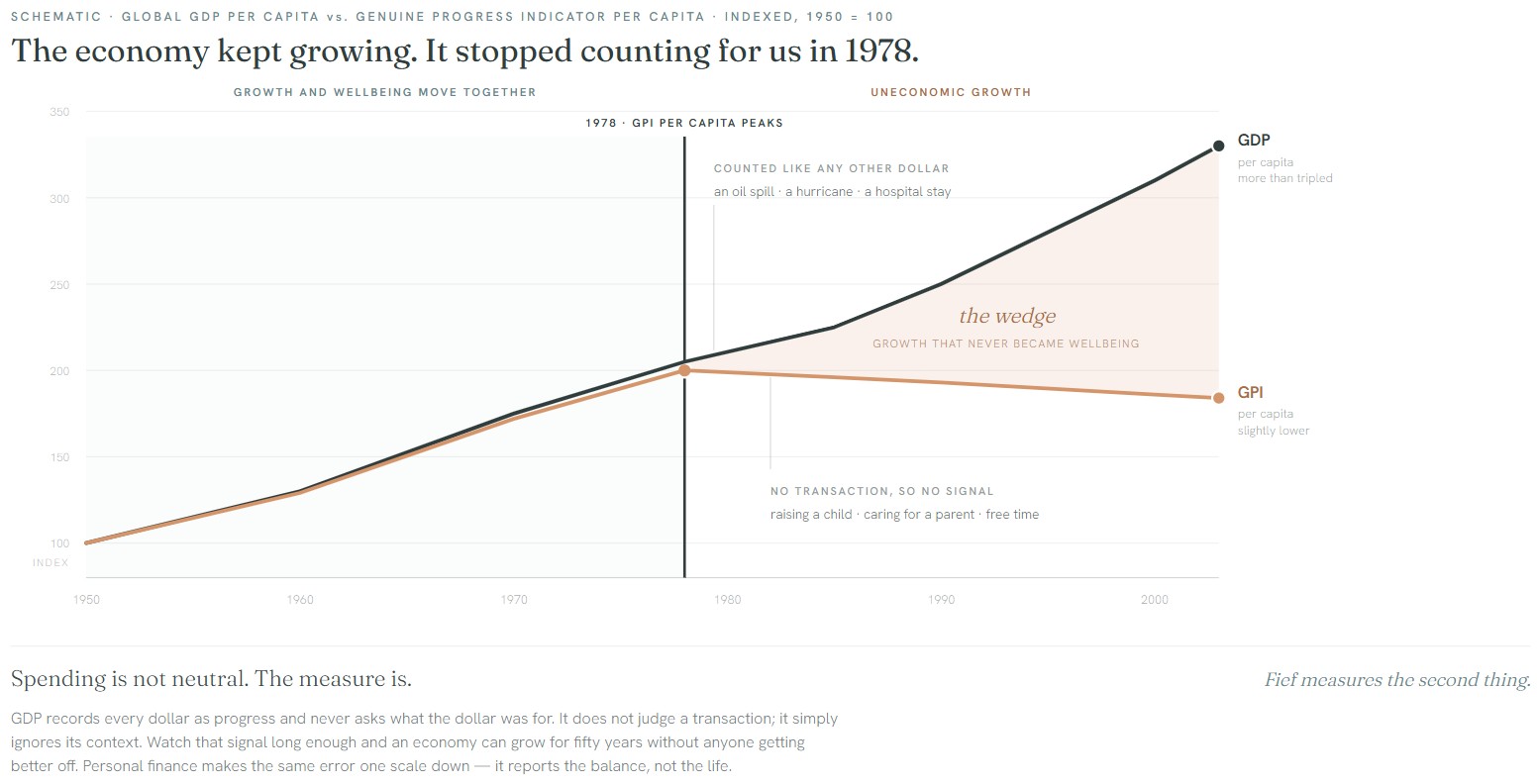

A GPI for one person

The capability lens isn't new — it's the Genuine Progress Indicator, scaled down. Since 1995 the GPI has offered a corrective to GDP: it adjusts for inequality, unpaid work, and environmental harm to measure whether people are actually better off, not just whether activity went up. It's been taken up at the state level — including here in Vermont — and applied across more than seventeen countries.

Fief runs that same logic at the scale of one person: money measured by what it builds, not what it totals. And because those individual patterns aggregate — anonymized and consented — they feed back up into the civic picture. The loop closes: one life and the system it sits in, measured the same way.

The spine that everything is supported by

Four depth levels — co-created onboarding, a working layer where goals, abilities, and financial state stay separate and never collapse into one “score,” a personal capabilities spider, and a collective ecosystem spider — with two flows: inputs down, roadmap up.

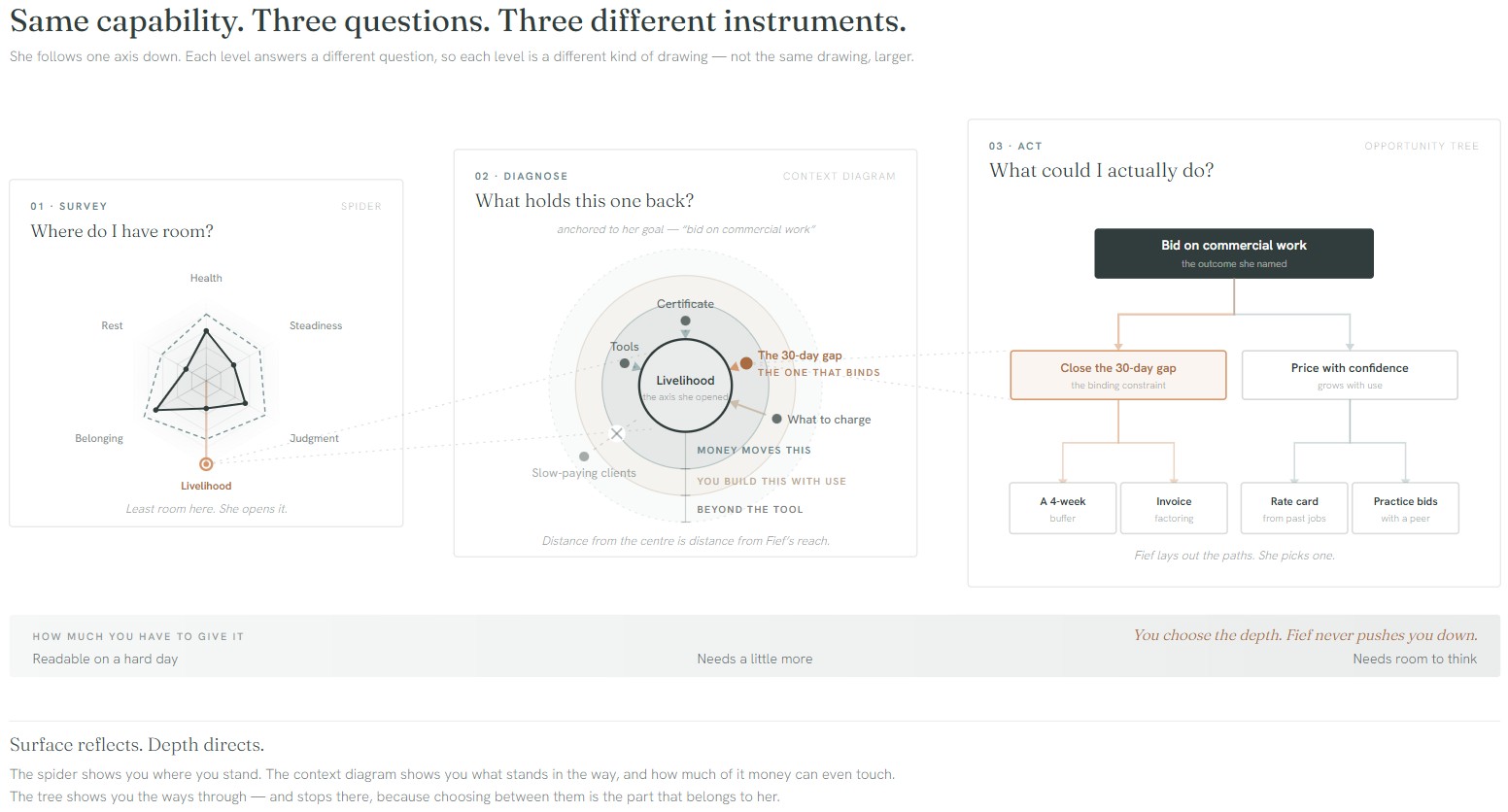

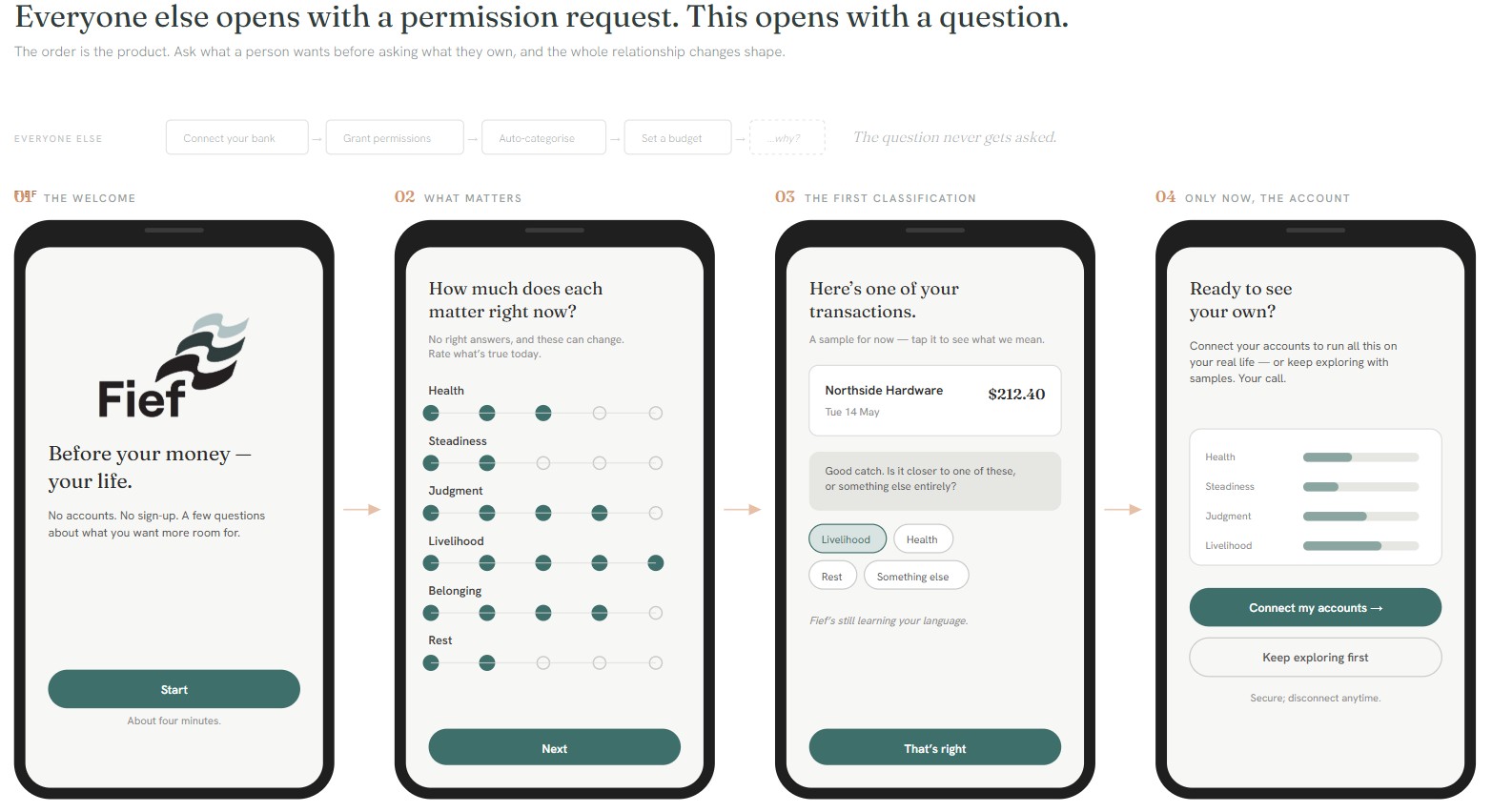

The North Star instrument is one spider at three zoom levels — survey the whole map, diagnose the axis that's gating you, act on the next capability-linked move. Onboarding holds one rule: values before accounts, always — Plaid connects last, not first. And the co-navigator surfaces through two rhythms: Compass Flow for the everyday, and Re-Calibration — a no-red-numbers, three-question recovery — when life diverges from plan.

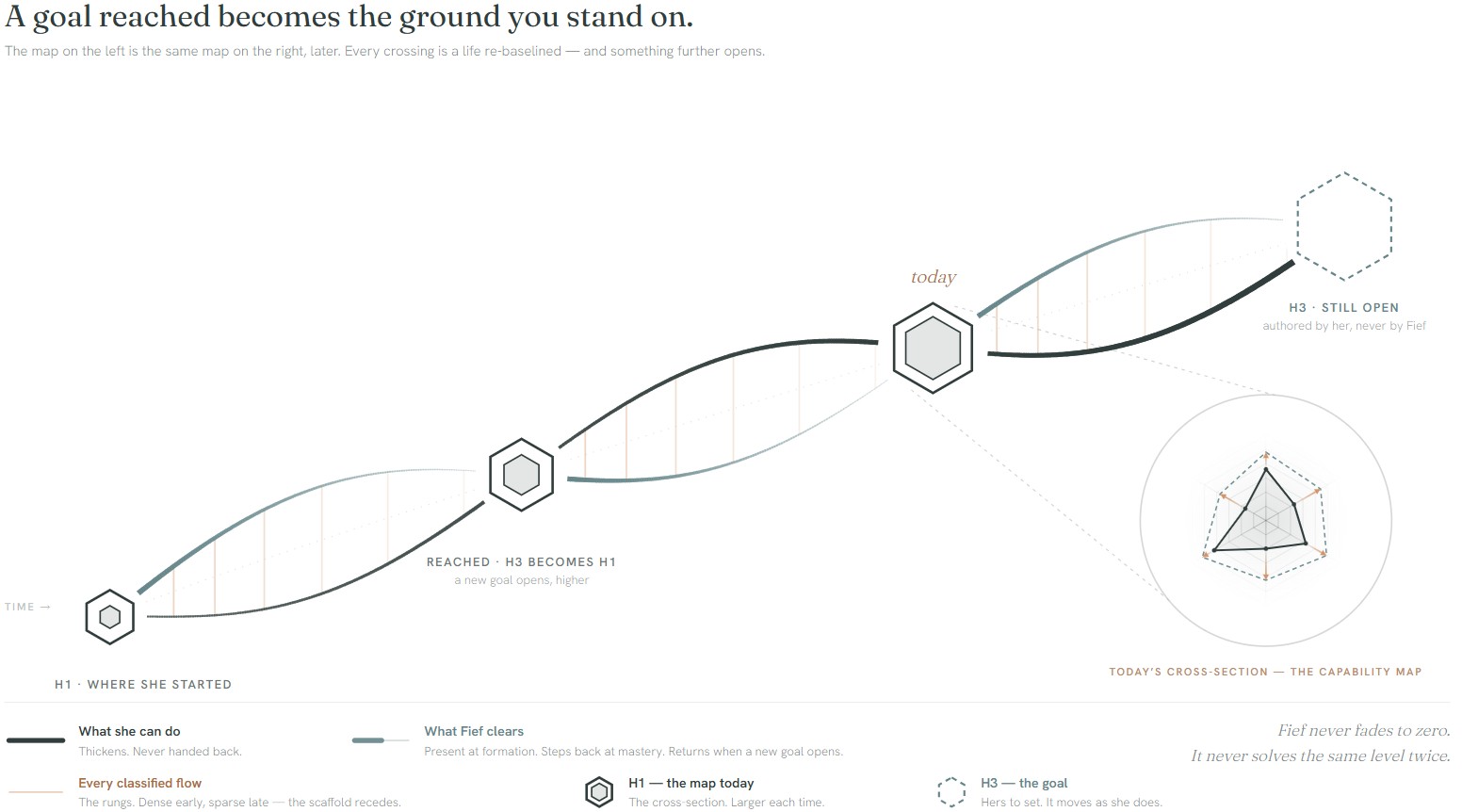

That gap is structured with the Three Horizons framework — where you are today (Horizon 1), where you want to be (Horizon 3), and the bridge between them (Horizon 2). The actionable part is Horizon 2: Fief sequences it into concrete next moves, so the brief stops being a wish and becomes a staged roadmap you can act on this week.

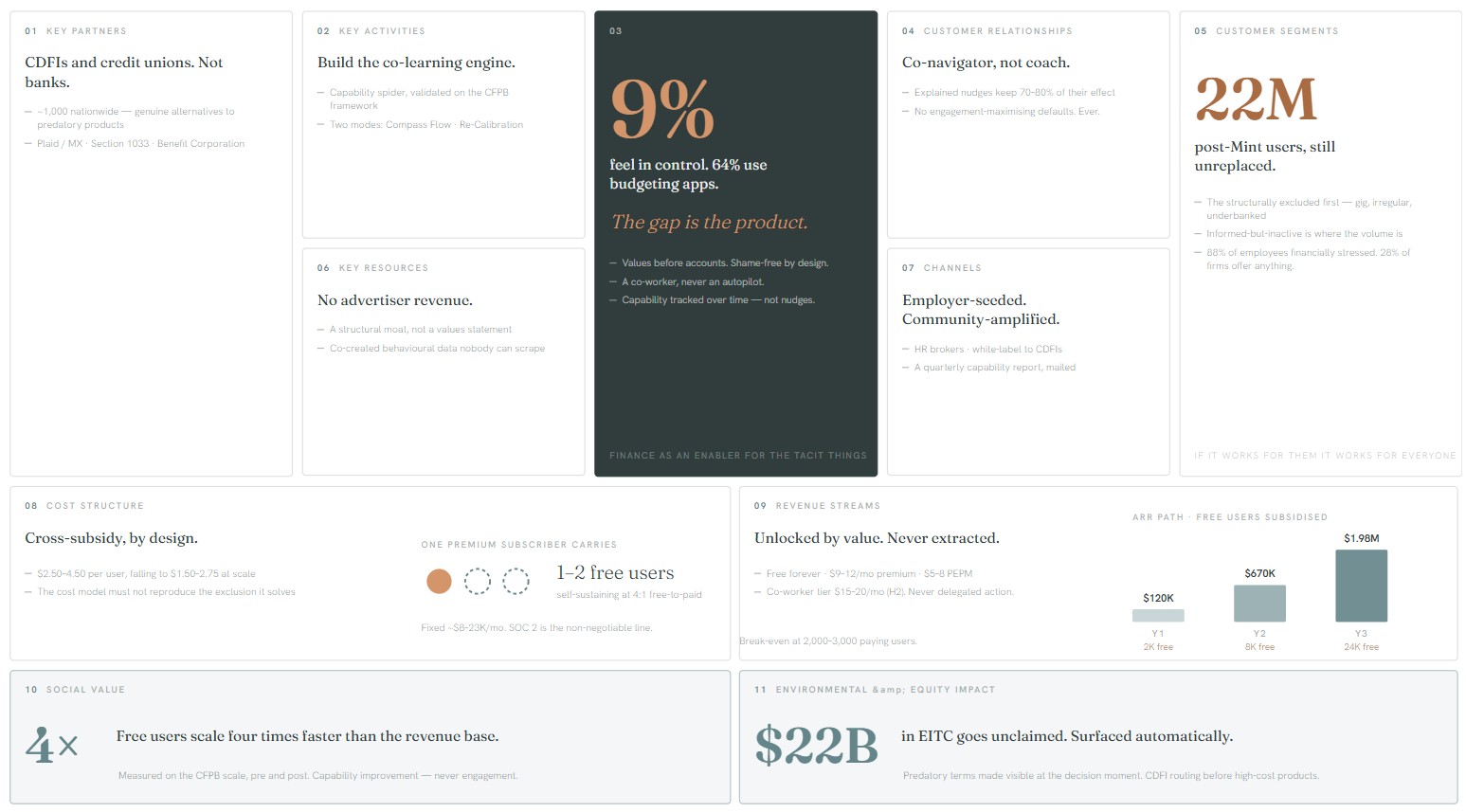

Make the equity structural, not charitable

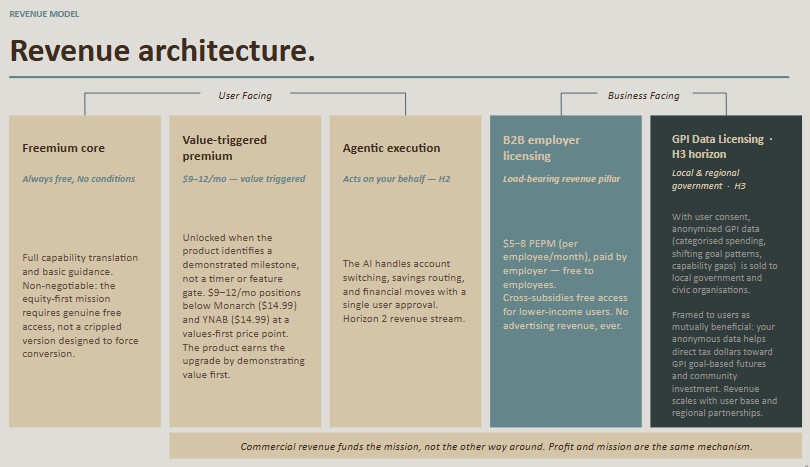

Revenue is value-triggered and fiduciary-aligned: a genuinely free core, a $9–12 premium unlocked only at a demonstrated milestone (below YNAB and Monarch), load-bearing B2B employer licensing, and consented, anonymized civic data — no advertising, ever.

Equity by design

At a 4:1 free-to-paid ratio, one 500-seat employer client funds 670–1,200 free users. The mission and the model are the same mechanism.

Prove → attract → rewire

The same three-horizon logic, one scale up — prove the model now (H1), attract the people and partners (H2), rewire the system (H3). Fief is Horizon 1, and its commercial success is the argument for the rest.

Unit economics and ARR are modeled estimates, pre-revenue.